Why I Bought Constellation Software

Full CSU investment thesis

A year ago I started studying serial acquirers. The idea behind this model appealed to me immediately: a company that can reinvest all of its free cash flow into new acquisitions at high returns. For me as a quality investor, that is one of the most powerful forms of value creation.

When executed well, a company like this can keep growing for years. Not because the market cooperates on its own, but because management actively keeps allocating capital to new, profitable businesses. Over the long run, that can create an enormous amount of value for shareholders.

In my search I quickly came across Constellation Software. The company that put the serial acquirer model in software on the map by acquiring countless VMS businesses. At the helm stands Mark Leonard, widely regarded as the Warren Buffett of the software industry. His reputation within the sector is almost mythical.

Yet at the time I decided not to go further with the company. The reason was simple: valuation. The stock was trading well above 5,000 Canadian dollars, with a P/FCFA above 50. However strong the business was, the quality was fully priced in. That did not feel comfortable to me.

Constellation kept coming back in my research into other serial acquirers nonetheless. In annual reports, shareholder letters, and investor calls, the company was frequently cited as an example. CEOs spoke with admiration about Mark Leonard and the model he has built. Companies like Kelly Partners Group and Röko openly refer to Constellation. The influence is clearly felt throughout the space.

Then the company faded into the background again, until weeks ago, when a broad SaaS selloff took place. Constellation was hit too. The stock halved to approximately 2,400 Canadian dollars, and the P/FCFA dropped to around 25 on a trailing basis, roughly 35 based on 2024 figures. That changed my perspective. What was previously too expensive suddenly looked attractive. The P/FCF is even lower!

Fundamentally I always found the business strong. The structure, the market, the financials, and the management were never in question for me. Valuation was the sticking point. Now that obstacle has partly disappeared, this felt like the right moment to take a fresh look.

Note: i wrote this post a few weeks ago, before the earnings. So prices and cashflow i use, can be a bit outdated.

In this post I take you through my thought process toward an investment thesis for Constellation Software.

I have since opened a small position of 4 percent, a so-called library card. That gives me greater involvement and motivation to understand the business even better. There are still uncertainties, but with a small position I can continue to explore whether this is a company I would feel comfortable with over the long term.

A free subscription is very much appreciated as support.

Why I Bought Constellation Software

In this post I am not going into detail on all the fundamentals of the business, the market, management, specific threats, or the full business model. I see that as the groundwork of an investment thesis. A thesis is really about summarizing earlier findings and clearly articulating the core of the investment.

In a full deep dive I would cover those elements extensively. You would look at market structure, competitive position, capital allocation, risks, and all the other building blocks needed to fully understand a business.

If you want to do your own further research on Constellation Software, I recommend reading the deep dive by TacticzHazel. He has published a comprehensive and free analysis that clearly explains all the important aspects of the company. That forms a solid foundation for forming your own informed view.

When you are looking for businesses that can keep growing year after year, you often end up at companies with a strong compounding model. These are businesses that do not distribute or sit on the earnings they generate today, but reinvest them at high returns. As a result, earnings grow not linearly but at an accelerating pace. The value for shareholders can therefore increase exponentially over long periods of time.

Serial acquirers, in the right hands, can be exceptionally powerful compounders. Every acquisition adds earnings and cash flow directly. That additional cash flow is then deployed into new acquisitions. This creates a flywheel that reinforces itself. The larger the company becomes, the more capital it can reinvest, and the stronger the compounding effect.

Constellation Software is one of the most compelling examples of this model. Since its IPO, the company has compounded at roughly 30 percent per year. That kind of result does not arise by chance, but through years of discipline in capital allocation and consistent execution of the model.

Mark Leonard led Constellation for many years. For health reasons he recently stepped down as CEO. That news came unexpectedly. Leonard remains active on the board and still holds a significant equity stake in the company. His financial interests therefore remain fully aligned with those of other shareholders.

The timing of his departure was unfortunate. Shortly before it, Constellation gave an investor presentation on the potential threat of AI, something the company rarely does. That was immediately followed by news of his stepping down. The market placed those events side by side and assumed the worst. The stock was promptly sold off sharply.

I could easily fill pages on Mark Leonard and what he has built. His discipline, his shareholder letters, and the fact that for years he took only one dollar in salary. But ultimately, an investment is not about nostalgia. It is about the future of the business.

Still, I felt it was important to briefly address Leonard’s role in this thesis. He was the architect of the model and the culture. But Constellation is by now larger than any one person, and that is precisely where the focus now needs to be.

The successor to Mark Leonard is not an outsider. Mark Miller has been closely involved with the company for more than thirty years and was Leonard’s right hand throughout. He helped build Constellation and knows the model, the culture, and the acquisition strategy inside and out. His experience within the sector and his involvement in countless acquisitions make him, in my view, a logical choice.

What matters to me is that this does not appear to be a radical change in direction. Miller is not known as someone who wants to reinvent the model. On the contrary, he helped shape it himself. That gives confidence that the discipline in capital allocation and the focus on niche VMS businesses will be maintained.

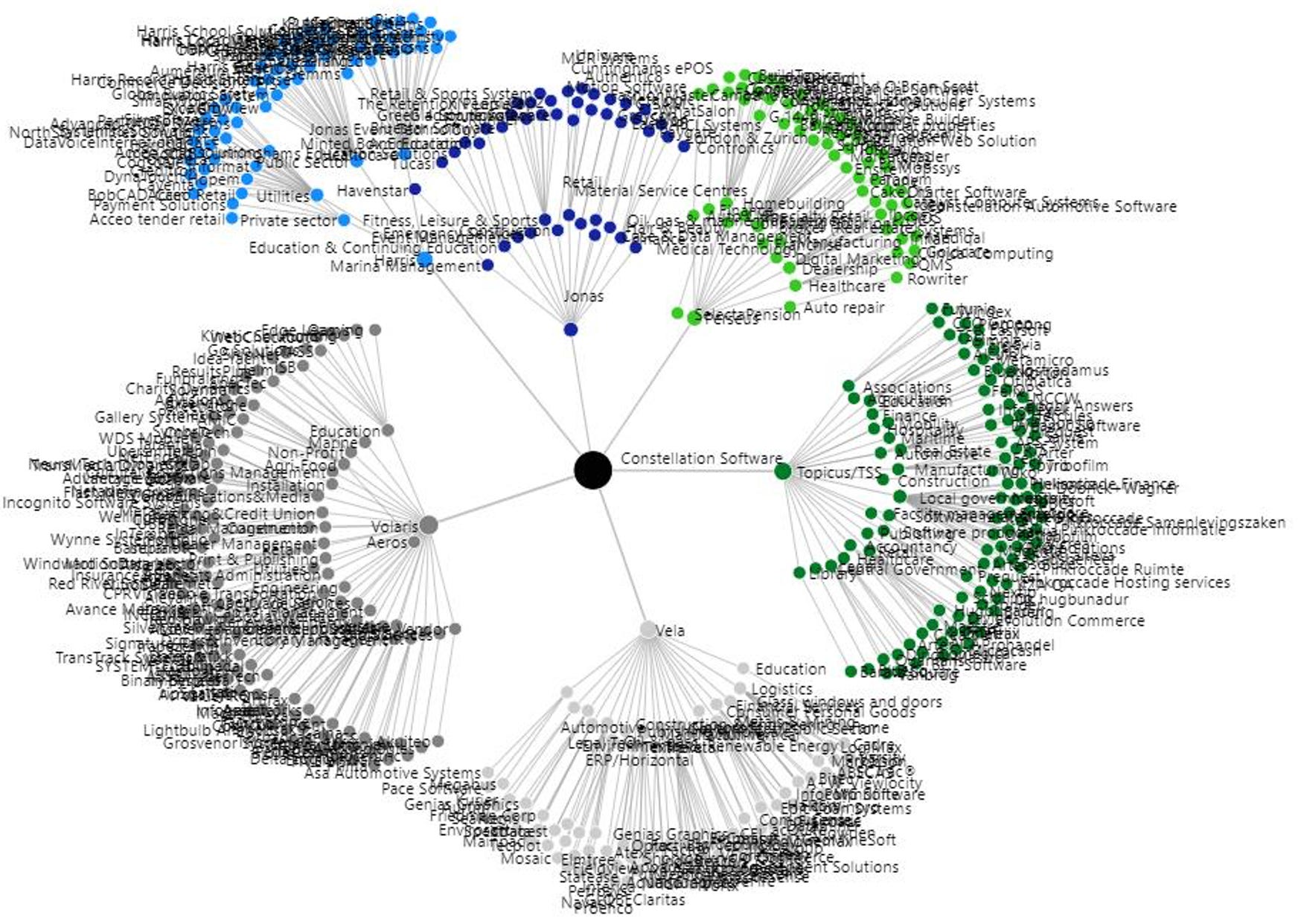

I also have a strong impression that Mark Leonard has deliberately worked over the past years to minimize his own central role. Constellation is not built around a single charismatic leader who makes all decisions. The company is divided into six independent operating groups, each responsible for hundreds of small software businesses. These groups operate largely autonomously.

It is precisely this structure that makes the company less dependent on any one person. Leonard was important as a cultural carrier and capital allocator, but the system does not run on his day-to-day involvement. That makes the transition to Miller, in my view, far less risky than the market initially appeared to think.

Acquisitions at Constellation are not driven centrally from headquarters. They are approved and executed by the managers of the individual platforms. That was a deliberate choice by Mark Leonard. He structured the company to allow maximum autonomy and independence within the different units. In this way bureaucracy is limited and decisions stay close to the market.

This decentralized model is one of the strongest characteristics of Constellation. The people with the best visibility into a niche market are also the ones making acquisition decisions within that niche. Headquarters sets the framework and guards capital discipline, but does not involve itself in every individual deal.

That is precisely why I expect the departure of Mark Leonard to change very little operationally. Strategy is set at a high level by the CEO, but execution is distributed throughout the organization. Under Miller I am confident the same course will be maintained as in recent years. The culture, the structure, and the capital allocation are deeply embedded. The timing of Leonard’s departure may be unfortunate, especially during a period of market volatility, but the impact on day-to-day operations seems limited to me. Through the strong autonomy of the platforms, the foundation of the business remains intact.

What Does Constellation Software Actually Do?

At its core, the model is simple. Constellation buys vertical market software businesses, so-called VMS companies, and holds them forever. The free cash flow those businesses generate is then reinvested into new acquisitions. It is a compounding machine that runs on reinvestment at high returns.

Like other preferred acquirers in this space, many owners would rather sell to Constellation than to private equity. Private equity typically buys with the intention of selling again within a few years. Costs are cut tightly and the business is optimized for an exit. Constellation does the opposite. It keeps businesses permanently, leaves management in place, and integrates them within one of its six platforms. That creates continuity and trust among sellers.

The businesses Constellation acquires provide mission-critical software in small niches. Think of software for bus routes, systems for bowling alleys, or software that tracks the number of chickens on a poultry farm. It can sound trivial, but for the customer it is crucial. This software typically represents around one percent of the total cost structure of the customer. Yet it is essential for daily operations. Switching to an alternative carries risks that simply do not justify the limited cost savings.

The total market per niche is also often small. The TAM is limited, which means large software companies are rarely interested. Constellation specifically acquires businesses that already hold a strong position within such a niche. That means little direct competition and high customer retention.

Globally there are estimated to be more than 20,000 such businesses whose owners are looking for a clean exit. Constellation typically targets companies with revenues of 2 to 5 million euros and applies an internal hurdle rate above 25 percent ROIC. By consistently repeating this, the company can keep growing over a long period of time.

Constellation has also recently taken platforms such as Topicus and Lumine public. It retains a large stake in both. This allows Constellation to benefit indirectly from their further growth, while freeing up capital for new acquisitions.

Constellation has four revenue streams. License revenue makes up 3.8%. Professional services, which includes upgrades, training, and installation for customers, accounts for 18.7%. Hardware and other is 3%. Maintenance is the most important at 74.46%, this is the revenue that flows from the SaaS model, where companies pay monthly to use the software of Constellation’s portfolio businesses.

The Risks That Pushed the Stock Down Hard

There are a number of clear reasons why the stock has declined so sharply.

The first is the departure of Mark Leonard as CEO. That news came unexpectedly for many investors and immediately created uncertainty. Leonard is after all the face of Constellation and seen as the architect of its success. I have already addressed this risk above and consider the operational risk limited. The culture, the capital allocation, and the decentralized model are deeply embedded in the organization. The timing is unfortunate, but the foundation of the company does not rest on one person alone.

The second reason is the AI narrative. Over the past few weeks, the suggestion has been made with increasing frequency that AI could be disruptive for software businesses. With a few smart prompts, almost anyone can now build a simple software program using tools like Claude or other AI models. That raises a logical question: if software is becoming easier to build, what is the remaining value of existing software companies?

Honestly, I find this a difficult subject to assess with certainty. Developments are moving at a rapid pace. Anyone who now claims to know exactly which companies will win or lose from AI is overestimating themselves. Technological changes are following each other so quickly that it is simply not reliably predictable, with the exception of the most direct hardware providers.

The market also frequently overestimates how quickly change occurs. Consider the cloud: that transition has been underway since 2007, yet many companies still run their IT on-premise.

For Constellation I see no direct existential threat in the near term. The businesses they own typically provide mission-critical software. Think of systems for governments, public infrastructure, and other essential processes. In many cases the software accounts for only a small percentage of the total cost structure, sometimes around one percent. The incentive to switch to a slightly cheaper or marginally better AI-built alternative is therefore limited. The risks of switching are simply too great relative to the savings. The incentive to build a replacement software system using AI is also low, given the small TAM.

Over the long term, AI could of course mean structural change. The range of possible outcomes is wide. But at this point I see it more as an opportunity than as a direct threat. The negative sentiment is pushing software company valuations down, which actually makes it more attractive for Constellation to make acquisitions. The company can also integrate AI into its existing software and position itself to benefit from technological development rather than be caught off guard by it.

The third risk, and for me the biggest near-term concern, is that the larger free cash flow makes future growth harder. This is also why I still hold a relatively small position. The cash flows of Topicus and Chapters are much smaller, meaning their growth runways are considerably longer. I deliberated for a long time between Chapters, Topicus, and Constellation for this reason. I will briefly explain this risk and why I ultimately chose Constellation first, since the position is still a library card, I can always decide to move to one of the other two if I do not feel comfortable with the position over time.

Constellation Software has, through its many acquisitions, grown very large. It generates more than 2 billion in free cash flow available for acquisitions. The organic growth of Constellation has historically been no more than 3% due to the low TAM and saturated markets of its portfolio businesses. Growth must therefore come from acquiring new businesses at a high hurdle rate. With 2 billion in free cash flow and an average acquisition price of 5 million, you need to acquire a very large number of small businesses annually just to keep growing. That is where investor anxiety lies. The business needs new acquisitions to grow, and if it cannot fully reinvest its cash flow, growth can stall.

Since 2022, the number of acquisitions by Constellation has clearly declined. Management itself acknowledges that this was largely due to the high valuations of SaaS businesses during that period. That was also visible in the market. Quality was scarce and being sold at high multiples.

At the same time, Constellation’s free cash flow kept growing. That puts the company in front of a choice: reinvest that cash flow in more acquisitions, or in larger ones? The latter route has now been taken. Constellation is buying larger businesses, but also acknowledges that the ROIC on these transactions is typically lower than on smaller VMS businesses. That is simply due to higher purchase prices.

Doing more small acquisitions sounds attractive, but there is a practical constraint. Each business must be thoroughly assessed for quality. That takes time and capacity. Yet the acquisition pipeline is still large, especially now that SaaS valuations have declined. There are therefore still sufficient opportunities, though a portion of them will be in larger deals with a somewhat lower ROIC.

Another interesting possibility is building a new platform outside of VMS. Mark Leonard hinted at this in the past. He once mentioned the idea of acquiring oil companies back in 2008. That did not happen, but it shows that Constellation does not necessarily need to restrict itself to vertical market software. If the company actually takes that step, a much larger acquisition pool opens up. The key question remains what the return on invested capital would be. The CEO of Röko recently noted that VMS has historically generated the highest ROIC.

Constellation could also choose minority stakes in publicly listed businesses (it does now). Leonard has previously expressed admiration for Veeva. It is therefore not unthinkable that part of the free cash flow flows into this type of participation. Chapters Group already does this. That remains speculative, but it shows that multiple strategic options exist. The company can also take new platforms public, as it did with Topicus.

For me, the reinvestment question is the biggest near-term risk. Yet I believe Constellation has sufficient options to navigate it. Management has a proven track record and the acquisition pool remains large, both within and potentially outside of VMS.

There are also alternatives such as Topicus and Chapters. Topicus, a European VMS platform within Constellation, has a longer runway due to its smaller free cash flow. Yet I find the structure complex. Via Constellation, which owns over 30 percent and may increase that stake, you indirectly also have exposure to that longer runway. That feels simpler to me.

Chapters has an even longer runway, but also carries higher debt and less proven management. The potential return is higher, but so is the risk. Constellation by contrast has a strong balance sheet, substantial cash, limited debt, and no goodwill on the balance sheet. It is conservatively financed and managed by a proven team. That is why my preference for now lies with Constellation.

When Would I Sell?

No investment is without risk. However strong the Constellation model is, there are clear signals that would lead me to reconsider my thesis. Below are the most important things I watch for, with some additional context.

Higher customer churn, the first real AI threat

If AI genuinely becomes disruptive for the niche VMS businesses of Constellation, it will show up in the numbers. Think declining maintenance revenue or a clear deceleration in organic revenue growth. Maintenance in particular is crucial: it represents recurring, predictable income from mission-critical software.

If this revenue structurally declines and management explicitly acknowledges that this is driven by AI or increasing competition, that is a serious warning signal for me and reason to reconsider my position.

Difficulty reinvesting free cash flow

The compounding model lives and dies by reinvestment at high returns. Constellation currently reinvests approximately 90% of its free cash flow, down from around 100% previously. According to management, this is largely due to high SaaS valuations. I consider that a valid reason: overpaying lowers ROIC and undermines the hurdle rate, something Constellation has historically guarded strictly.

If this is temporary, it is not a problem. But if the company structurally struggles to deploy its cash flow productively while opportunities do exist, the alarm bells ring. If management then comes with a thoughtful solution, for example expanding into new sectors while maintaining high ROIC, that is acceptable. But if it opts for large acquisitions at low returns simply to deploy capital, that undermines the model and would be a potential sell signal for me.

A more attractive alternative

Finally: if Topicus, Chapters, or another serial acquirer proves structurally more attractive, whether through a longer runway, better capital allocation, or a better risk/reward, reallocation could make sense. Capital should work where it generates the best returns.

In short, my confidence in Constellation is high, but not unconditional. The model is powerful as long as the core principles, low churn, high ROIC, and disciplined capital allocation, remain intact. Once those change, so does my judgment.

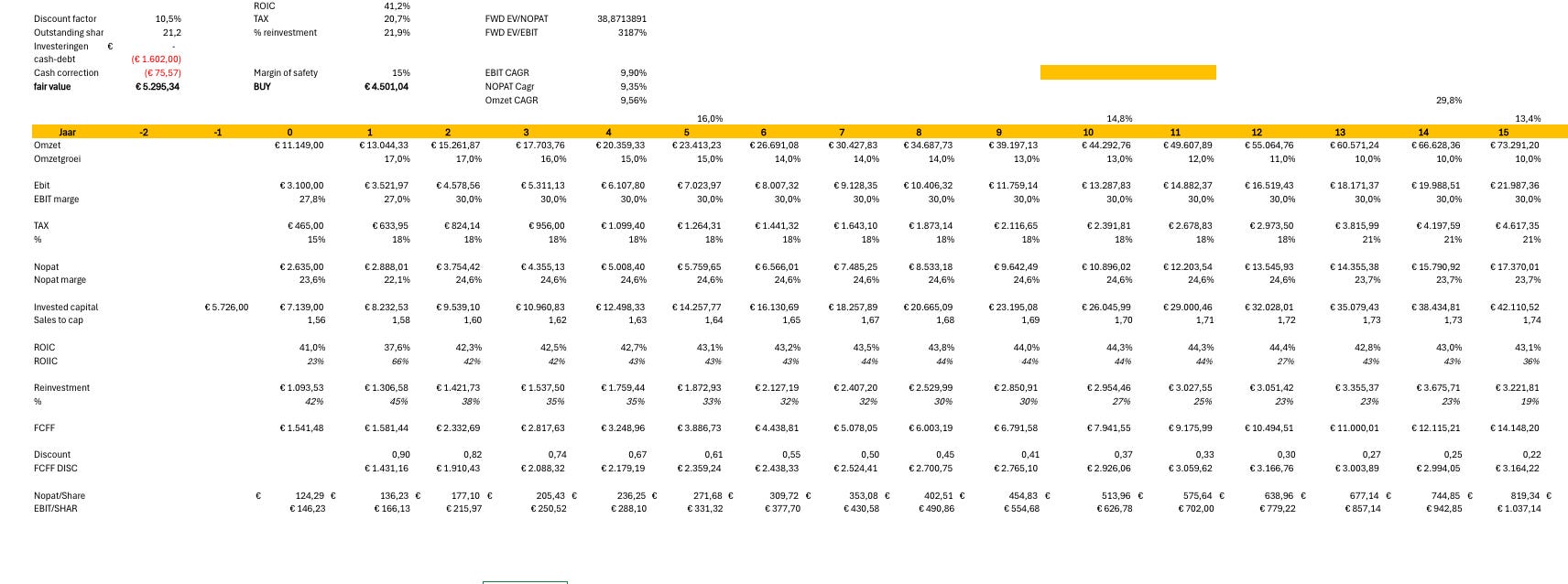

Valuation

Now the most important part: the valuation.

As I mentioned, Constellation has always traded at a premium. The market for years saw it as an exceptional quality business, and a high multiple came with that. A few weeks ago that picture changed dramatically. At the time of writing, the stock has declined 53% to 2,280 Canadian dollars.

These are the historical growth figures for Constellation Software. Thanks to its unique business model, continuously reinvesting free cash flow at high returns, the company can in theory sustain these growth figures for a long time. In practice that becomes more challenging as the acquisition pool narrows, as discussed earlier.

I will approach the valuation in two ways. The market at the current price is only pricing in approximately 12% FCFA growth, which seems on the pessimistic side. For the first valuation method I therefore work with a P/FCFA multiple that I consider justified, deliberately using a modest multiple so the outcome is not too dependent on optimistic valuation assumptions.

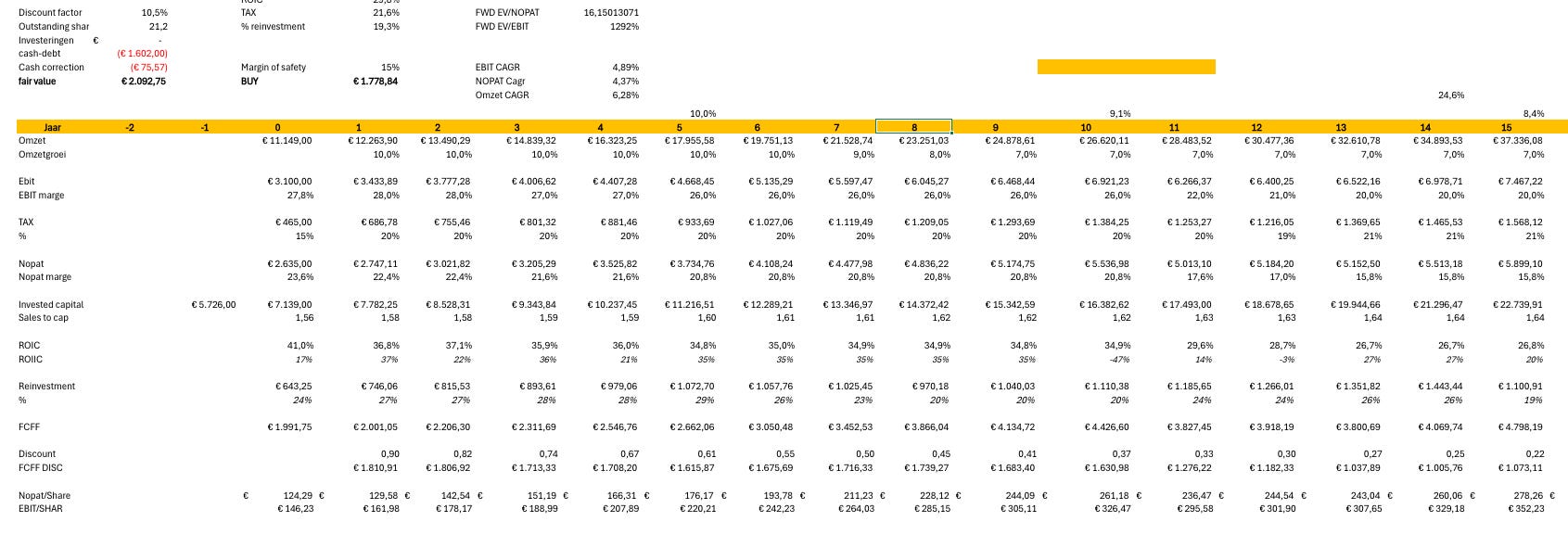

The second method is a DCF model. Here I start from EBITA, because that gives a better picture of the underlying profitability of Constellation than EBIT. Constellation acquires many businesses and writes down these acquisitions through amortization. These are however not cash expenses, but purely accounting costs. Because acquisitions form the very core of the business model, I correct for this by working with EBITA.

From EBITA I subtract the tax charge to arrive at NOPAT. I then subtract reinvestments to arrive at FCFF. Those reinvestments depend on the ROIC. In my model I let the ROIC gradually decline, because Constellation will likely need to do larger acquisitions, where returns are typically somewhat lower than on smaller deals.

I work this out in a bear, base, and bull case. I move through them fairly quickly, since I have already discussed the key risks in detail above.

Bear Case

Over 2024 the P/FCFA is 33 at the current price. Based on estimated 2025 FCFA of approximately 1,700 Canadian dollars, the P/FCFA is only 26, while the historical average sits around 50. There is significant margin variation, but the 10-year average FCFA margin is around 16.7%.

In the bear case I assume rapidly declining revenue growth, with falling margins and a declining valuation. The business is hurt by the AI threat and cannot fully reinvest its cash flow at a lower ROIC. Revenue growth decelerates while AI pressures pricing power and the FCFA margin drops to just 12%.

The P/FCFA stabilizes at 20. The stock price over 15 years would come out at approximately 3,923 Canadian dollars. This would deliver an annual return of just 3.43% per year, well below market average.

The average EBITDA margin is 25.72%, though this has been increasing meaningfully in recent years.

In the bear case I assume margins come under pressure from declining pricing power. In all scenarios I use a required return of 10.5%. Given the AI threat and the reinvestment risk, I want an additional premium in my required return.

I keep revenue growth constant, but let the EBITDA margin gradually decline to 20% over 15 years. The tax rate rises to 25% and ROIC falls to 25%.

On these assumptions, the fair value comes out at 2,092 Canadian dollars. Around the current share price, this means that even in this bear scenario you could still expect a return of approximately 10% per year. Of course, in the event of genuine disruption, where revenue actually starts to decline, outcomes could be considerably worse.

Base Case

In the base case I deliberately choose a conservative and realistic approach. As Constellation gets larger, it becomes mathematically harder to maintain the same high growth percentages. I therefore assume the company does fewer acquisitions but finds new ways to continue reinvesting its free cash flow efficiently.

Revenue growth in this scenario is clearly below the historical average of over 20% per year. I initially model average growth of 12.5%, which then slows to 9%. This aligns with the law of large numbers. I keep the FCFA margin slightly below the historical average of 16.7%, at 16%.

Although the current P/FCFA is historically low, I do not assume multiple expansion in this scenario. I therefore use a P/FCFA of 35, which is historically still on the low side for Constellation. This way the return is based not on market sentiment, but purely on the underlying strength of the business.

With these assumptions the IRR comes out to a solid 13%, and that based on relatively conservative starting points.

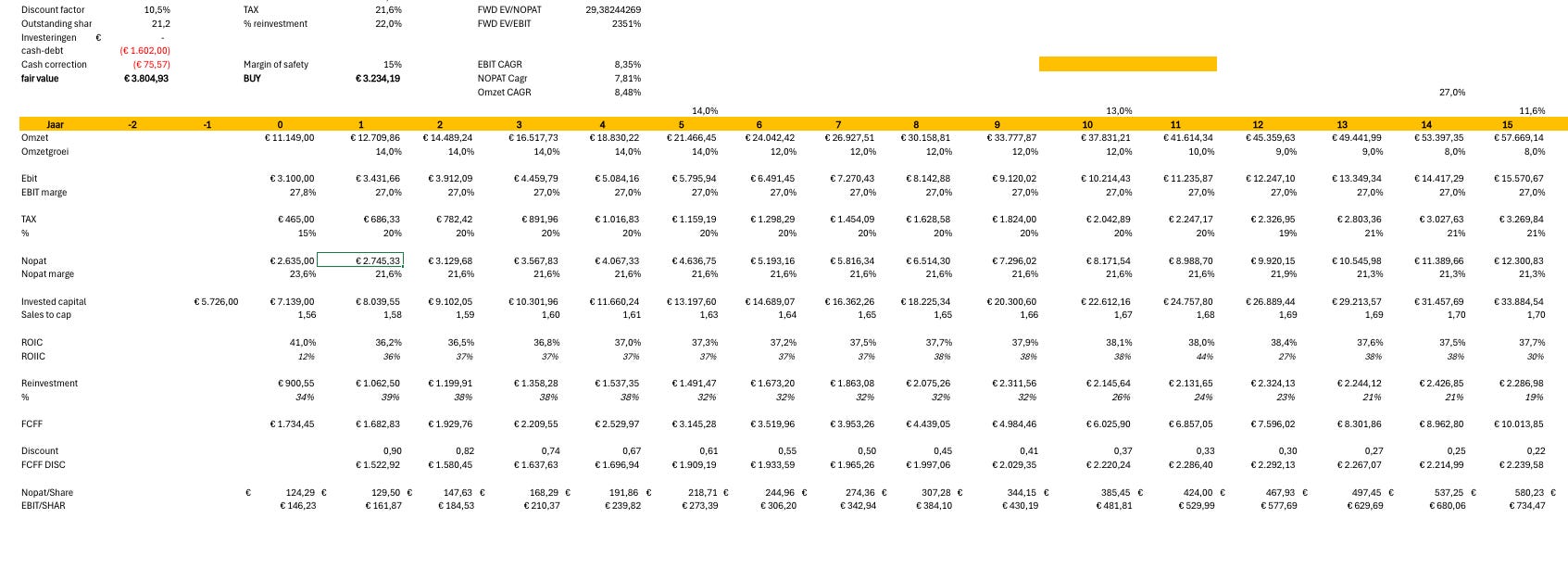

For the DCF I use the same revenue growth assumptions as in the base case. I model an EBITDA margin of 27% and a tax rate of 20%. This keeps ROIC stable at around 37%. Margins are slightly lower than historical in this scenario, because larger acquisitions are typically done at lower returns than smaller deals.

On these assumptions I arrive at a fair value of over 3,800 Canadian dollars per share, well above the current price. In this scenario a return of approximately 13.5% per year appears achievable based on a DCF, which I see as the purest form of valuation. And all of this within a reasonably conservative base case.

Bull Case

In the bull case I assume Constellation manages to largely continue its historical compounding model. That means the company continues to efficiently reinvest its free cash flow at high returns, despite the larger scale. The acquisition pool remains large enough and management finds ways to structure even larger deals at attractive returns.

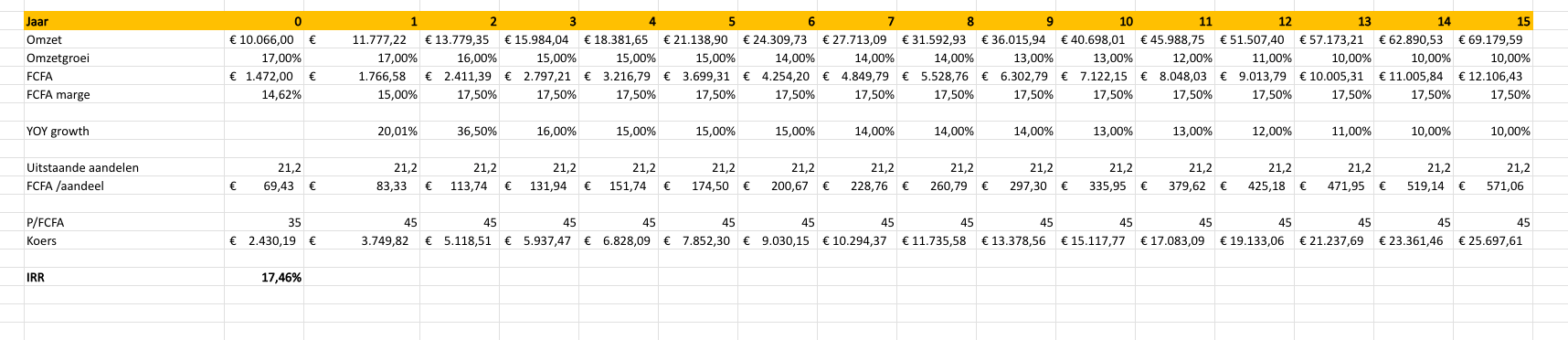

Revenue grows in this scenario at around 17% per year in the early years, gradually declining to 10% by year 15. That is still very strong for a company of this size, but more realistic than the historical growth rate of over 20%.

The FCFA margin expands to 17.5% and stays there. The company is able to use AI to operate more efficiently.

Free cash flow per share grows in this scenario from approximately 69 to over 571 Canadian dollars by year 15. That is an eightfold increase over fifteen years. I use a P/FCFA of 45, which is not a high multiple historically for Constellation, but does reflect recognition of the quality and predictability of the model. This scenario therefore assumes a revaluation of the company.

On these assumptions the share price grows from approximately 2,430 to over 25,600 Canadian dollars by year 15. That implies an IRR of approximately 17.5% per year.

For this scenario much needs to go right: the reinvestment pace must remain high, AI must not cause structural damage to the underlying VMS businesses, and management must maintain its capital allocation quality. If that happens, Constellation remains an exceptional compounder even from the current price.

For the DCF, EBITDA margins rise to 30% through efficient deployment of AI. ROIC rises to 44%. With these ambitious revenue growth assumptions, the fair value comes out at 5,300 Canadian dollars, good for a return of 15.75%.

Short Thesis

Constellation is an exceptional quality business with a unique compounding model. It buys mission-critical VMS businesses, holds them forever, and reinvests virtually all free cash flow at high returns. For decades this has led to impressive value creation for shareholders. Management’s capital discipline is exceptional, the balance sheet is strong, and the culture of autonomy within the platforms makes the model scalable and robust.

Yet the range of possibilities has clearly widened. The greatest uncertainty lies with AI. In the near term I see limited threat, because the software is typically mission-critical and represents only a small portion of customer costs. But over the long term the impact of AI is hard to predict. There is also the reinvestment risk: if Constellation needs to do larger deals at lower ROICs, or struggles to deploy capital efficiently, compounding can slow.

Valuation has now fallen substantially. The business today needs to perform far less well than it has historically to still deliver an attractive return. That makes the stock fundamentally interesting. At the same time, the downside toward a real bear case is greater than the upside toward the bull case, precisely because uncertainty has increased and growth will become harder.

I am therefore keeping this a smaller position. Should the stock decline another 10 to 15 percent, I would consider adding. I would consider selling if organic growth structurally declines due to higher churn, if management acknowledges that AI is genuinely eroding pricing power, or if capital is being redeployed at clearly lower returns without a convincing strategic rationale.

Constellation remains one of the best businesses in its category, but due to the wider range of outcomes I am not comfortable with a large position.

There is an enormous amount of material available on the company. I particularly recommend the deep dive by TacticzHazel alongside the Speedwell Research podcast with Drew Cohen and the annual letters of Mark Leonard to learn far more about the business.

Thank you for reading. Do not forget to subscribe and like the post

Very interesting ! If you haven’t yet come across @James Stawicki in this space, I can’t recommend you enough to read his latest analysis on TOI and the new PEMS analysis within the CSU universe!